TABLE OF CONTENTS

| Topics | Sections |

|---|---|

| OVERVIEW | 6.1 What is the purpose of this chapter? 6.2 What is the scope of this chapter? 6.3 What are the authorities for this chapter? 6.4 What is the overall Service policy? 6.5 What terms do you need to know to understand this chapter? |

| RESPONSIBILITIES | 6.6 What are the responsibilities for Environmental and Disposal Liability (EDL) reporting? 6.7 When should Service officials consult with the Department’s Office of the Solicitor? |

| REQUIREMENTS | 6.8 What is the process flow for EDL review and reporting? 6.9 What are the requirements for reporting EDLs? 6.10 When are EDL updates due? |

| GUIDANCE | 6.11 What guidance should Project Managers follow to identify, record, and report EDLs? |

OVERVIEW

6.1 What is the purpose of this chapter? This chapter provides policy and procedures for U.S. Fish and Wildlife Service (Service) employees reporting information on Environmental and Disposal Liability (EDL). Following the requirements in the chapter ensures we report accurate, timely, and consistent EDL information to the Department of the Interior (Department).

6.2 What is the scope of this chapter? This chapter applies to all Service employees involved with EDL reporting.

6.3 What are the authorities for this chapter?

A. Chief Financial Officers Act of 1990 (Public Law 101-576).

B. Department’s Environmental and Disposal Liabilities Handbook v4.0.

C. Federal Accounting Standards Advisory Board (FASAB):

(1) Statement of Federal Financial Accounting Standards (SFFAS):

(a) SFFAS No. 5, Accounting for Liabilities of the Federal Government;

(b) SFFAS No. 6, Accounting for Property, Plant, and Equipment (PP&E); and

(c) SFFAS No. 54, Leases: An Amendment of SFFAS 5, Accounting for Liabilities of the Federal Government and SFFAS 6, Accounting for PP&E.

(2) Technical Bulletins:

(a) 2006-1, Recognition and Measurement of Asbestos-Related Cleanup Costs;

(b) 2009-1, Deferral of the Effective Date of Technical Bulletin 2006-1, Recognition and Measurement of Asbestos-Related Cleanup Costs; and

(c) 2011-2, Extended Deferral of the Effective Date of Technical Bulletin 2006-1, Recognition and Measurement of Asbestos-Related Cleanup Costs.

(3) Federal Financial Accounting and Auditing Technical Releases:

(a) Technical Release 2, Determining Probable and Reasonably Estimable for Environmental Liabilities in the Federal Government;

(b) Technical Release 10, Implementation Guidance on Asbestos Cleanup Costs Associated with Facilities and Installed Equipment;

(c) Technical Release 11, Implementation Guidance on Cleanup Costs Associated with Equipment; and

(d) Technical Release 14, Implementation Guidance on the Accounting for the Disposal of General Property, Plant, and Equipment.

D. Government Management Reform Act of 1994 (Public Law 103-356).

F. OMB Circular No. A-136, Financial Reporting Requirements.

6.4 What is the overall Service policy? We must:

A. Provide accurate and timely EDL information to the Department, and

B. Include all estimated future costs for cleanup resulting from past or current operations that have:

(1) Environmental closure requirements (e.g., solid waste landfills; treatment, storage, or disposal facilities; and mine sites); or

(2) A release of hazardous substances, pollutants, or contaminants for which we are responsible by law or statute.

6.5 What terms do you need to know to understand this chapter?

A. Balance sheet is a statement of the financial standing of an entity that lists the assets, liabilities, and net position at a particular point in time.

B. Contingency is an existing condition, situation, or set of circumstances involving uncertainty as to a possible gain or loss that will ultimately occur or fail to occur. Per FASAB standards, we only report loss contingencies.

C. Disclosure is information we present in notes that is an integral part of the basic financial statements. A disclosure should include the nature of the contingency and an estimate of the total range of potential liability. We do not include disclosed EDLs in the calculation of the recognized EDL amount.

D. Due care is the process we follow to make a reasonable effort to examine a potential EDL site to identify the presence or likely presence of contamination at concentrations significant enough to require further study or cleanup. An environmental professional must perform or oversee this process.

E. Environmental and Disposal Liability (EDL) is the future outflow or other sacrifice of resources where, based on the results of due care, we anticipate further study or cleanup of contamination is warranted due to past or current operations. The Department’s EDLs comprise two types of liability: environmental remediation liabilities and asbestos cleanup liabilities. We report these liabilities as EDLs on the balance sheet, but we disclose them separately in the note to the financial statements on the Department’s Agency Financial Report (AFR).

F. EDL database is an information technology system designed to record and track environmental remediation liabilities throughout the Department.

G. Generally Accepted Accounting Principles (GAAP) are a collection of commonly followed accounting rules and standards for financial reporting. The specifications of GAAP, which is the standard adopted by the U.S. Securities and Exchange Commission, include definitions of concepts and principles, as well as industry-specific rules. The purpose of GAAP is to ensure that financial reporting is transparent and consistent from one organization to another. The American Institute of Certified Public Accountants Council designated FASAB as the body that establishes GAAP for Federal entities.

H. Government-acknowledged financial responsibility is when a Government entity did not cause or contribute to the contamination and is not otherwise liable for cleanup costs, but the Government chooses to accept financial responsibility to protect public health, welfare, or the environment. The cleanup costs are considered Government acknowledged, and in these situations we only disclose cleanup costs.

I. Liability, for Federal financial accounting purposes, is a probable and measurable future outflow or other sacrifice of Service or Departmental resources (e.g., costs) as a result of past events or transactions. This definition is in Federal accounting standards. Reporting a financial liability does not imply or infer acceptance of legal liability.

RESPONSIBILITIES

6.6 What are the responsibilities for Environmental and Disposal Liability (EDL) reporting? See Table 6-1.

Table 6-1: Responsibilities for EDL Reporting

| These employees… | Are responsible for… |

|---|---|

| A. The Director | Approving or declining to approve Servicewide policy. |

| B. Directorate members (i.e., Regional Directors; Assistant Directors; Director, National Conservation Training Center (NCTC); Chief, National Wildlife Refuge System (NWRS)) | Delegating their authority to the Regional Environmental Compliance Coordinator (RECC), or other appropriate personnel, to review and approve site-specific EDL information for their Region or program. |

| C. Assistant Director – Management and Administration (i.e., AD-MA or Associate Chief Financial Officer) | Ensuring EDL amounts are appropriately recorded in the body and footnotes of the Service’s financial statements. |

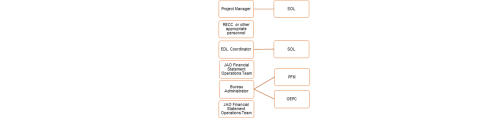

| D. NWRS, Infrastructure Management Division Deputy Chief (i.e., Bureau Administrator) | (1) Ensuring that Service employees who are responsible for reviewing EDL information for each site do so, (2) Documenting their (i.e., Bureau Administrator) review of site information in the EDL database and informing the Department’s Office of Environmental Policy and Compliance (OEPC) and the Office of Financial Management (PFM) that the update is complete, and (3) Informing the Joint Administrative Operations (JAO) Financial Statement Operations team that the Infrastructure Management Division’s review is complete. |

| E. NWRS, Infrastructure Management Division, EDL Coordinator (within the Branch of Environmental Compliance and Sustainability) | (1) Performing the final technical review of EDL projects we list in the EDL database, (2) Documenting their review and approval in the EDL database, (3) Informing the JAO Financial Statement Operations team that their review is complete, and (4) Consulting with the Department’s Office of the Solicitor (SOL) as required (see section 6.7). |

| F. Regional Environmental Compliance Coordinators (RECC), or other appropriate personnel | (1) Exercising their delegated authority to review and approve site-specific EDL information for their Region or program, (2) Reviewing EDL information for sites in their Region or program and documenting that review in the EDL database, (3) Ensuring that the appropriate cost estimate documentation is included in the site information, (4) Verifying that the SOL has reviewed projects as required, and (5) Notifying the EDL Coordinator when they (i.e., the RECC) complete the review. |

| G. Joint Administrative Operations (JAO), Administrative Operations Center (AOC), Financial Statement Operations Team | (1) Reviewing financial statements to ensure that the EDL information conforms to applicable accounting standards, (2) Developing footnote references and journal entries for the Service’s quarterly and annual financial reports to the Department, (3) Responding to inquiries from Service employees about accounting issues that impact financial reporting, and (4) Documenting their review in the EDL database and informing the Bureau Administrator that the review is complete. |

| H. Project Managers | (1) Identifying sites for EDL reporting, (2) Preparing accurate cost estimates for projects, (3) Obtaining review from the SOL of new projects and changes to existing projects that may affect liability estimates (see section 6.7), (4) Entering site-specific information into the EDL database for new sites and updating information for existing sites, and (5) Informing their RECC or other appropriate Regional/program personnel that the information is ready for review. |

6.7 When should Service officials consult with the Department’s Office of the Solicitor? As we describe in Table 6-1, the appropriate Service official must consult with SOL, or verify that staff have consulted with SOL, to determine:

A. The status of legally binding agreements, orders, or other third-party commitments to pay or perform work; and

B. Whether there are any new projects or changes to existing projects that may affect liability estimates.

REQUIREMENTS

6.8 What is the process flow for EDL review and reporting? See Figure 6-1.

Figure 6-1: Flow Diagram of EDL Review and Reporting Process

6.9 What are the requirements for reporting EDLs?

A. OMB requires the Department and other Federal agencies to:

(1) Prepare annual audited financial statements in accordance with the Chief Financial Officers Act of 1990 and the Government Management Reform Act of 1994, and

(2) Submit quarterly, unaudited financial statements in accordance with OMB Circular A-136. Agencies must report information on EDLs in these financial statements.

B. The Department’s PFM office requires us to update EDLs at least annually. We update EDLs in the EDL database each quarter.

6.10 When are EDL updates due?

A. First, Second, and Third Quarters: The reports are due to the Department 1 week prior to the end of the first, second, and third quarters. We should update and approve data for those quarters according to the timeline in Table 6-2:

Table 6-2: Timeline for Updating, Reviewing, and Approving EDL Data

| This employee… | Should do this… | At least this many weeks before the end of each quarter… |

|---|---|---|

| Project Manager | Add and update information in the EDL database and notify the RECC or other appropriate personnel. | 5 weeks |

| RECC or other appropriate personnel | Review and approve Regional EDL information and notify the EDL Coordinator. | 4 weeks |

| EDL Coordinator | Review and approve EDL database information and notify the JAO Financial Statement Operations team. | 3 weeks |

| JAO Financial Statement Operations team | Review and approve EDL database information and notify the Bureau Administrator. | 2 weeks |

| Bureau Administrator | Review and approve EDL database information and notify the Department that the data are final. | 1 week |

B. Fourth Quarter: If an update that significantly changes the information occurs during the fourth quarter, the EDL information is due to the Department 2 weeks before the end of the quarter. The process for updating, reviewing, and approving fourth quarter information should begin 1 week earlier than we describe in section 6.10A.

GUIDANCE

6.11 What guidance should Project Managers follow to identify, record, and report EDLs? Project Managers should follow the guidance in the Department’s Environmental and Disposal Liabilities Handbook. The handbook provides information on:

A. Identifying EDLs,

B. Determining liability status,

C. Estimating EDL costs, and

D. Recording and reporting EDLs.